FTSMA - Trend is your frendThis my new solid strategy: if you belive that "TREND IS YOUR FRIEND" this is for you!

I have tested with many pairs and at many timeframes and have profit with just minor changes in settings.

I suggest to use it for intraday trading .

VERY IMPORTANT NOTE: this is a trend following strategy, so the target is to stay in the trade as much as possible. If your trading style is more focused on scalping and/or pullbaks, this strategy is not for you.

This strategy uses moving averages applied to Fourier waves for forecasting trend direction.

How strategy works:

- Buy when fast MA is above mid MA and price is above slow MA, which acts as a trend indicator.

- Sell when fast MA is below mid MA and price is below slow MA, which acts as a trend indicator.

Strategy uses a lot of pyramiding orders because when you are in a flat market phase it will close 1 or 2 orders with a loss, but when a big trend starts, it will have profit in a lot of orders.

So, if you analize carefully the strategy results, you will note that "Percent Profitable" is very low (30% in this case) because strategy opened a lot of orders also in flat markets with small losses, BUT "Avg # bars in winning trades" is very high and overall Profit is very high: when a big trend starts, orders are kept open for long time generating big profits.

Thanks to all pinescripters mentioned in the code for their snippets.

I have also a study with alerts. Next improvement (only to whom is interested to this script and follows me): study with alerts on multiple tickers all at one. Leave a comment if you want to have access to study.

HOW TO USE STRATEGY AND STUDY TOGHETER:

1- Add to chart the strategy first, so your workspace will be as clean as possible.

2- Open the Strategy Tester tab at footer of the page.

3- Modify settings to get best results (Profit, Profit Factor, Drawdown).

4- Add study with alerts to your chart with same setting of strategy.

I WILL PROVIDE A DETAILED QUICK INSTALLATION GUIDE WITH THE STUDY!

Please use comment section for any feedback or contact me if you need support.

Cerca negli script per "the strat"

Combo Backtest 123 Reversal & ECO Strategy This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

We call this one the ECO for short, but it will be listed on the indicator list

at W. Blau’s Ergodic Candlestick Oscillator. The ECO is a momentum indicator.

It is based on candlestick bars, and takes into account the size and direction

of the candlestick "body". We have found it to be a very good momentum indicator,

and especially smooth, because it is unaffected by gaps in price, unlike many other

momentum indicators.

We like to use this indicator as an additional trend confirmation tool, or as an

alternate trend definition tool, in place of a weekly indicator. The simplest way

of using the indicator is simply to define the trend based on which side of the "0"

line the indicator is located on. If the indicator is above "0", then the trend is up.

If the indicator is below "0" then the trend is down. You can add an additional

qualifier by noting the "slope" of the indicator, and the crossing points of the slow

and fast lines. Some like to use the slope alone to define trend direction. If the

lines are sloping upward, the trend is up. Alternately, if the lines are sloping

downward, the trend is down. In this view, the point where the lines "cross" is the

point where the trend changes.

When the ECO is below the "0" line, the trend is down, and we are qualified only to

sell on new short signals from the Hi-Lo Activator. In other words, when the ECO is

above 0, we are not allowed to take short signals, and when the ECO is below 0, we

are not allowed to take long signals.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & ECO This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

We call this one the ECO for short, but it will be listed on the indicator list

at W. Blau’s Ergodic Candlestick Oscillator. The ECO is a momentum indicator.

It is based on candlestick bars, and takes into account the size and direction

of the candlestick "body". We have found it to be a very good momentum indicator,

and especially smooth, because it is unaffected by gaps in price, unlike many other

momentum indicators.

We like to use this indicator as an additional trend confirmation tool, or as an

alternate trend definition tool, in place of a weekly indicator. The simplest way

of using the indicator is simply to define the trend based on which side of the "0"

line the indicator is located on. If the indicator is above "0", then the trend is up.

If the indicator is below "0" then the trend is down. You can add an additional

qualifier by noting the "slope" of the indicator, and the crossing points of the slow

and fast lines. Some like to use the slope alone to define trend direction. If the

lines are sloping upward, the trend is up. Alternately, if the lines are sloping

downward, the trend is down. In this view, the point where the lines "cross" is the

point where the trend changes.

When the ECO is below the "0" line, the trend is down, and we are qualified only to

sell on new short signals from the Hi-Lo Activator. In other words, when the ECO is

above 0, we are not allowed to take short signals, and when the ECO is below 0, we

are not allowed to take long signals.

WARNING:

- For purpose educate only

- This script to change bars colors.

MTF Trailing SL Alerts [QuantNomad]These are alerts for my MTF Trailing SL Strategy.

Entry Long position if all 4 time-frames agree on the long signal.

Exit Long positions when at least 2 time-frames disagree on the long signals.

Entry to Short position if all 4 time-frames agree on Short signal.

Exit from Short positions when at least 2 time-frames disagree on Short signal.

Use "Once Per Bar Close" when creating alerts.

Link to the strategy:

Combo Backtest 123 Reversal & Ease of Movement (EOM) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator gauges the magnitude of price and volume movement.

The indicator returns both positive and negative values where a

positive value means the market has moved up from yesterday's value

and a negative value means the market has moved down. A large positive

or large negative value indicates a large move in price and/or lighter

volume. A small positive or small negative value indicates a small move

in price and/or heavier volume.

A positive or negative numeric value. A positive value means the market

has moved up from yesterday's value, whereas, a negative value means the

market has moved down.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Ease of Movement (EOM) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator gauges the magnitude of price and volume movement.

The indicator returns both positive and negative values where a

positive value means the market has moved up from yesterday's value

and a negative value means the market has moved down. A large positive

or large negative value indicates a large move in price and/or lighter

volume. A small positive or small negative value indicates a small move

in price and/or heavier volume.

A positive or negative numeric value. A positive value means the market

has moved up from yesterday's value, whereas, a negative value means the

market has moved down.

WARNING:

- For purpose educate only

- This script to change bars colors.

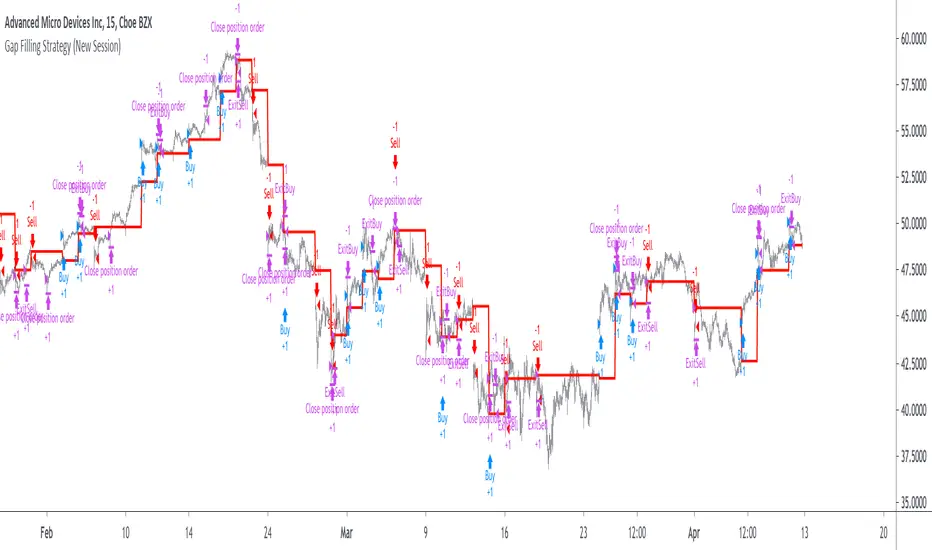

Gap Filling Strategy Gaps are market prices structures that appear frequently in the stock market, and can be detected when the opening price is different from the previous closing price, this is why gaps are also called "opening price jumps". While gaps can occur frequently, some of them are more significant than others, and can be observed when looking at a long term chart.

The following strategy is based on the exploitation of significant gaps occurring during a new session, and posses various options that can return a wide variety of results.

Type Of Gaps And Occurence

I'am not a professional when it comes to gaps, but as you know the stock market close for the day, however it is still possible to place orders, your broker will hold them until the market open back. Once the market reopen the broker execute the pending orders, and when many orders where pending the market register really high volume and the price might differ from the precedent close.

Gaps are generally broken down into four types:

Common : Gaps occurring within a certain price range, mostly occurs during ranging markets.

Break Away : Gaps breaking a support and resistance, making a new higher high/lower low.

Runaway : Gaps occurring within a trend, followed by a continuation of the trend.

Exhaustion : Gaps occurring at the end of a trend, followed by a reversal.

As said before, some gaps are more significant than others, the significance of a gap can be determined by comparing the opening price with the previous high/low price and by looking at volume. Significant up gaps will have an opening price greater than the previous high, while significant down gap will have an opening price lower than the previous low with both high volume accompanying them.

After a gap, when the price go back to the point previous to the gap we say that it has been "filled", this characteristic is what will be exploited in this strategy.

Strategy Rules & Logic

In this strategy, the significance of a gap is determined by the position of the opening price relative to the previous high/low and make sure the bar following the gap don't fill it.

When the setting invert is set to false the strategy interpret the detected gaps as being exhaustion gaps, therefore when an up gap occur a short position is opened, when a down gap occur a long position is opened. When invert is set to true gaps are considered to be runaway or break away gaps, therefore the contrary positions are opened. Positions are exited when the gap has been filled, which in the chart is show'n when the price cross the red level who act as either a take profit (invert = false) or as a stop loss (invert = true).

There are various closing conditions available that the user can select from the "close when" setting.

New Session : This option close all previous positions when the market is in a new session.

New Gap : This option close all previous position when a new gap has been detected.

Reverse Position : This option close all previous position when a contrary position to the current one is opened. This option would reduce the number of trades.

Testing On Some Stocks

The analysis will be tested in different tech stocks with a main TF of 15 minutes with no spread and commissions applied. Default settings will be used. We'll be making our first analysis using AMD, who has recently formed a full reverse HS pattern, where the neckline has been crossed by the price. (by the way i have a bad feeling about it, hey ! feeling filling ! Lame jokes!)

Profit: $ -12.22

Trades: 272

Profitability: 65.07 %

We can see negative results, with an heavily decreasing balance. Using invert would return positive results.

We will now test the strategy on NVDA, the company is one of the biggest when it comes to the Gpu market.

Profit: $ -215.54

Trades: 297

Profitability: 60.27 %

Not better, using invert would of course create better results. Like AMD the balance is heavily decreasing.

Finally we will test the strategy on Seagate technology, a company mostly known for their mechanical hard drives.

Profit: $ -4.32

Trades: 261

Profitability: 65.9 %

Here the balance does not appear so heavily decreasing and even managed to reach back the initial balance before going down again.

Summary

A strategy based on gap filling has been briefly introduced and tested with 3 tech stocks. The results show that using invert option might be better. The advantage of this strategy against ones using technical indicators is that this one does not heavily depend on user settings, which make it way more efficient, this a big advantage of patterns based strategies.

Thx to LucF for helping with the "process_orders_on_close" element, since i had to use closing price i had to remove it tho, was afraid results would differ even more from a more realistic backtest. And thx for those who continuously support me, more cool stuff is coming up.

Thx for reading and i hope you'll have learned something new today !

Combo Backtest 123 Reversal & Dynamo This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

In July 1996 Futures magazine, E. Marshall Wall introduces the

Dynamic Momentum Oscillator (Dynamo). Please refer to this article

for interpretation.

The Dynamo oscillator is a normalizing function which adjusts the

values of a standard oscillator for trendiness by taking the difference

between the value of the oscillator and a moving average of the oscillator

and then subtracting that value from the oscillator midpoint.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & DynamoThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

In July 1996 Futures magazine, E. Marshall Wall introduces the

Dynamic Momentum Oscillator (Dynamo). Please refer to this article

for interpretation.

The Dynamo oscillator is a normalizing function which adjusts the

values of a standard oscillator for trendiness by taking the difference

between the value of the oscillator and a moving average of the oscillator

and then subtracting that value from the oscillator midpoint.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Dynamic Pivot Point This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This Pivot points is calculated on the current day.

Pivot points simply took the high, low, and closing price from the previous period and

divided by 3 to find the pivot. From this pivot, traders would then base their

calculations for three support, and three resistance levels. The calculation for the most

basic flavor of pivot points, known as ‘floor-trader pivots’, along with their support and

resistance levels.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Dynamic Pivot Point This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This Pivot points is calculated on the current day.

Pivot points simply took the high, low, and closing price from the previous period and

divided by 3 to find the pivot. From this pivot, traders would then base their

calculations for three support, and three resistance levels. The calculation for the most

basic flavor of pivot points, known as ‘floor-trader pivots’, along with their support and

resistance levels.

WARNING:

- For purpose educate only

- This script to change bars colors.

My VWAP Reversal + Pivot Points StandardThis indicator, with the addition of a standard VWAP indicator to the 5m chart, helps the operator when using a closing candle Price to initiate a VWAP Reversal strategy.

The strategy involves Price gapping up, look for a Close below the 1st 5m candle Low; else look for a Close above the 1st 5m candle High. On a break of VWAP, take the trade in the opposite direction of the gap, hence the VWAP Reversal. Not my own strat, credit to T3 Newsbeat, publicly posted on YouTube.

The Pivot Points Standard in the Pine 4 user manual, was the base source code, and leaving it here will allow me to remove the PP indicator I was using.

Combo Backtest 123 Reversal & Dynamic Momentum Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Dynamic Momentum Index indicator. The Dynamic Momentum

Index (DMI) was developed by Tushar Chande and Stanley Kroll. The indicator

is covered in detail in their book The New Technical Trader.

The DMI is identical to Welles Wilder`s Relative Strength Index except the

number of periods is variable rather than fixed. The variability of the time

periods used in the DMI is controlled by the recent volatility of prices.

The more volatile the prices, the more sensitive the DMI is to price changes.

In other words, the DMI will use more time periods during quiet markets, and

less during active markets. The maximum time periods the DMI can reach is 30

and the minimum is 3. This calculation method is similar to the Variable

Moving Average, also developed by Tushar Chande.

The advantage of using a variable length time period when calculating the RSI

is that it overcomes the negative effects of smoothing, which often obscure short-term moves.

The volatility index used in controlling the time periods in the DMI is based

on a calculation using a five period standard deviation and a ten period average

of the standard deviation.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Dynamic Momentum Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Dynamic Momentum Index indicator. The Dynamic Momentum

Index (DMI) was developed by Tushar Chande and Stanley Kroll. The indicator

is covered in detail in their book The New Technical Trader.

The DMI is identical to Welles Wilder`s Relative Strength Index except the

number of periods is variable rather than fixed. The variability of the time

periods used in the DMI is controlled by the recent volatility of prices.

The more volatile the prices, the more sensitive the DMI is to price changes.

In other words, the DMI will use more time periods during quiet markets, and

less during active markets. The maximum time periods the DMI can reach is 30

and the minimum is 3. This calculation method is similar to the Variable

Moving Average, also developed by Tushar Chande.

The advantage of using a variable length time period when calculating the RSI

is that it overcomes the negative effects of smoothing, which often obscure short-term moves.

The volatility index used in controlling the time periods in the DMI is based

on a calculation using a five period standard deviation and a ten period average

of the standard deviation.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & DSS Bressert This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Double Smoothed Stochastics (DSS) is designed by William Blaw.

It attempts to combine moving average methods with oscillator principles.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & DSS Bressert This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Double Smoothed Stochastics (DSS) is designed by William Blaw.

It attempts to combine moving average methods with oscillator principles.

WARNING:

- For purpose educate only

- This script to change bars colors.

Patient Trendfollower (7)(alpha)Patient Trendfollower consists of 21 and 55 EMA, Commodity Channel Index and Supertrend indicator. It confirms a trend and gives you a signal on a pullback. Original creation worked on 1h EURUSD chart.

►Long setup:

• 21 EMA is above 55 EMA, which is above the Supertrend indicator.

• Commodity Channel Index is an oscillator, which prints into the chart if extreme levels are reached. Green is for a level above 100 or below -100, red is above 140 or below -140 and black is above 180 or below -180.

• If 21 EMA > 55EMA > Supertrend and an oversold signal appear, you can buy into the trend.

• When backtesting on 1h EURUSD, profit target 400 pips worked best with a stop-loss below Supertrend's bottom and the size of your spread.

• A picture shows two valid entries.

: This part still malfunctions and shows red dots over some green ones. It is important to disable red ones in the settings to see green ones.

Some more long signals:

Some short signals:

►Backtesting data with default settings and trading only green CCI signals with mentioned risk management strategy:

• 212 closed trades

• 58.96% profitable with average win trade 348 USD and average loss trade 263 USD when only green signals are followed.

• Profit factor 1.903, Sharpee 0.792

• 20 bars is average for all trades, short trades were 18 bars long on average.

With given data, you can see the strategy is profitable by itself. However, original risk management settings do work only on 1h charts of EURUSD and would need to be adjusted for other instruments based on average volatility.

Even though the profitability is low, you can increase your odds by a great margin, if you properly use price action (impulsive and corrective moves, patterns, bar analysis), if you trade when major exchanges are open, you may also use wave analysis such as Elliot Waves or Market Profiles to predict whether the next day might be a trending day. My backtesting program didn't consider these ideas.

Unfortunately, I won't be making backtesting strategy public with it anytime soon, because it still has some parts that do not work. I am ok with that since I understand the code and know what does malfunction and how. Then, there are parts which I am not sure how to fix yet. This is why the indicator is still considered alpha.

In the future when a strategy is published, you will also be able to set your own overbought/oversold values without entering the code itself and probably some other features. But I am not in a hurry for that. You can give me feedback on UX and try to figure out the best setups for other symbols, it might help to improve the automatic testing script when I know what I should achieve. My main point is to make this public for friends who can already be using it on EURUSD at least.

Close doesn't always have to be 400 pips, you might want to close on a logical level such as strong resistance or a trendline too.

Thanks to:

• @everget for providing Supertrend solution.

• Satik FX who hand-tested the system by hand and reported results in this article . He is my main inspiration for creating the complete indicator as one because I want to be able to show and hide it with a single click. My future scripts will also work as a whole strategy each by itself.

• The number in the script's name comes from Satik's numbering. A mentioned article was his seventh shared strategy.

Combo Backtest 123 Reversal & Donchian Channel Width This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Donchian Channel was developed by Richard Donchian and it could be compared

to the Bollinger Bands. When it comes to volatility analysis, the Donchian Channel

Width was created in the same way as the Bollinger Bandwidth technical indicator was.

As was mentioned above the Donchian Channel Width is used in technical analysis to measure

volatility. Volatility is one of the most important parameters in technical analysis.

A price trend is not just about a price change. It is also about volume traded during this

price change and volatility of a this price change. When a technical analyst focuses his/her

attention solely on price analysis by ignoring volume and volatility, he/she only sees a part

of a complete picture only. This could lead to a situation when a trader may miss something and

lose money. Lets take a look at a simple example how volatility may help a trader:

Most of the price based technical indicators are lagging indicators.

When price moves on low volatility, it takes time for a price trend to change its direction and

it could be ok to have some lag in an indicator.

When price moves on high volatility, a price trend changes its direction faster and stronger.

An indicator's lag acceptable under low volatility could be financially suicidal now - Buy/Sell signals could be generated when it is already too late.

Another use of volatility - very popular one - it is to adapt a stop loss strategy to it:

Smaller stop-loss recommended in low volatility periods. If it is not done, a stop-loss could

be generated when it is too late.

Bigger stop-loss recommended in high volatility periods. If it is not done, a stop-loss could

be triggered too often and you may miss good trades.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Donchian Channel WidthThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Donchian Channel was developed by Richard Donchian and it could be compared

to the Bollinger Bands. When it comes to volatility analysis, the Donchian Channel

Width was created in the same way as the Bollinger Bandwidth technical indicator was.

As was mentioned above the Donchian Channel Width is used in technical analysis to measure

volatility. Volatility is one of the most important parameters in technical analysis.

A price trend is not just about a price change. It is also about volume traded during this

price change and volatility of a this price change. When a technical analyst focuses his/her

attention solely on price analysis by ignoring volume and volatility, he/she only sees a part

of a complete picture only. This could lead to a situation when a trader may miss something and

lose money. Lets take a look at a simple example how volatility may help a trader:

Most of the price based technical indicators are lagging indicators.

When price moves on low volatility, it takes time for a price trend to change its direction and

it could be ok to have some lag in an indicator.

When price moves on high volatility, a price trend changes its direction faster and stronger.

An indicator's lag acceptable under low volatility could be financially suicidal now - Buy/Sell signals could be generated when it is already too late.

Another use of volatility - very popular one - it is to adapt a stop loss strategy to it:

Smaller stop-loss recommended in low volatility periods. If it is not done, a stop-loss could

be generated when it is too late.

Bigger stop-loss recommended in high volatility periods. If it is not done, a stop-loss could

be triggered too often and you may miss good trades.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOaDisparity Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related CMOaDisparity Index article is copyrighted material from Stocks & Commodities Dec 2009

My strategy modification.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & CMOaDisparity Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related CMO Disparity Index article is copyrighted material from Stocks & Commodities Dec 2009

My strategy modification.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Directional Trend Index (DTI) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This technique was described by William Blau in his book "Momentum,

Direction and Divergence" (1995). His book focuses on three key aspects

of trading: momentum, direction and divergence. Blau, who was an electrical

engineer before becoming a trader, thoroughly examines the relationship between

price and momentum in step-by-step examples. From this grounding, he then looks

at the deficiencies in other oscillators and introduces some innovative techniques,

including a fresh twist on Stochastics. On directional issues, he analyzes the

intricacies of ADX and offers a unique approach to help define trending and

non-trending periods.

Directional Trend Index is an indicator similar to DM+ developed by Welles Wilder.

The DM+ (a part of Directional Movement System which includes both DM+ and

DM- indicators) indicator helps determine if a security is "trending." William

Blau added to it a zeroline, relative to which the indicator is deemed positive or

negative. A stable uptrend is a period when the DTI value is positive and rising, a

downtrend when it is negative and falling.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Directional Trend Index (DTI) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This technique was described by William Blau in his book "Momentum,

Direction and Divergence" (1995). His book focuses on three key aspects

of trading: momentum, direction and divergence. Blau, who was an electrical

engineer before becoming a trader, thoroughly examines the relationship between

price and momentum in step-by-step examples. From this grounding, he then looks

at the deficiencies in other oscillators and introduces some innovative techniques,

including a fresh twist on Stochastics. On directional issues, he analyzes the

intricacies of ADX and offers a unique approach to help define trending and

non-trending periods.

Directional Trend Index is an indicator similar to DM+ developed by Welles Wilder.

The DM+ (a part of Directional Movement System which includes both DM+ and

DM- indicators) indicator helps determine if a security is "trending." William

Blau added to it a zeroline, relative to which the indicator is deemed positive or

negative. A stable uptrend is a period when the DTI value is positive and rising, a

downtrend when it is negative and falling.

WARNING:

- For purpose educate only

- This script to change bars colors.